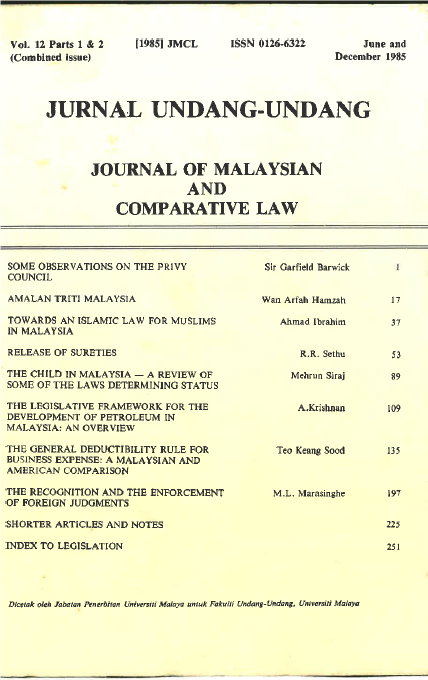

The General Deductibility Rule For Business Expense

A Malaysian And American Comparison

Keywords:

Income Tax 1967, Malaysian ActAbstract

Once a taxpayer has ascertained the amount of gross income, disputes frequently arise as to whether an expenditure incurred is an allowable item in computing the adjusted gross income. In Malaysia, the United States, taining adjusted gross income, certain express deductions and certain express or implied prohibitions of deduction must be taken into account. Where the expenditure is not spelt out either in the prohibiting section or in the section which allows specific deductions, it need not necessarily fall outside the scheme of deductions. As will be seen, if the outlay is a proper charge against income and fulfils ordinary principles of commercial trading, it is deductible.

Downloads

Published

2019-01-13

Issue

Section

Articles

How to Cite

The General Deductibility Rule For Business Expense: A Malaysian And American Comparison. (2019). Journal of Malaysian and Comparative Law, 12(1 and 2), 135-196. https://ijie.um.edu.my/index.php/JMCL/article/view/15956